20% Deduction for REITs and MLPs under the Tax Cuts and Jobs Act

The Tax Cuts and Jobs Act (TCJA) allows a 20% deduction for qualified business income (QBI) for pass-through businesses under Section 199A subject to certain limitations. The provision also allows for a 20% deduction for qualified REIT dividends and qualified publicly traded partnership (PTP) income. The deduction for REITs and PTPs is not subject to the limits imposed under QBI and as such a taxpayer can get a full deduction regardless of their income.

However, only a small portion of income from a REIT or PTP would qualify for the deduction. Most REITs and PTPs provide a return of capital every year which reduces the taxpayer’s basis in the investment and is not taxable. In case of a PTP, you can also have other deductions that would otherwise reduce the amount of income which would actually be taxed.

Examples of income distributed from a REIT or PTP that would not qualify for the deduction include:

Capital gains

Qualified dividends

Examples of income distributed from a REIT or PTP that would qualify for the deduction include:

Any income from the REIT or PTP’s business activities

Ordinary dividends (dividends that are taxed at ordinary rates)

Certain recapture income on the sale of a PTP

Each PTP is required to determine its qualified PTP income for each trade or business and report that information to its owners. A partner’s share of Section 199A income, qualified REIT dividends and qualified PTP income will be reported on box 20 of the Form 1065, Schedule K-1. Section 199A dividends from REITs will be reported on box 5 of the Form 1099-div. There is a 45 day holding period requirement surrounding the 91-days of the ex-dividend date in case of REIT dividends.

Qualified REIT dividends received from a mutual fund are eligible for a 20% deduction.

The Treasury and the IRS is considering how to treat qualified PTP/MLP income received from a mutual fund.

Finally, the total QBI deduction for the taxpayer cannot exceed the following:

20% X (Taxable income without QBI deduction – Net Capital Gain*)

This means that individuals with high capital gains and itemized deductions may not get the full 20% deduction.

*Net capital gains are calculated as follows:

Long-term capital gain

Plus qualified dividends

Less long-term capital losses

Less net short-term capital loss (the excess, if any, of STCL over STCG)

1. What is the provision in The Tax Cuts and Jobs Act?

For taxable years beginning after December 31, 2017 and before January 1, 2026, an individual taxpayer generally may deduct:

20% of qualified business income from a partnership, S corporation, or sole proprietorship, and;

20% of aggregate qualified REIT dividends, qualified cooperative dividends, and qualified publicly traded partnership (MLP) income.

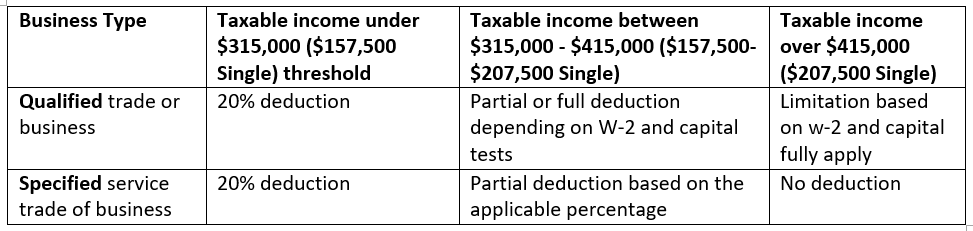

A limitation based on W-2 wages paid is phased in above a threshold amount of taxable income. A disallowance of the deduction with respect to specified service trades or businesses is also phased in above the threshold amount of taxable income.

Ignoring the limitations, an owner of a pass-thru business structure may now be taxed at a top rate of 29.6% (80% x 37%) as opposed to 39.6% under the old tax law. This results in a tax savings of 10%.

2. How does the formula work?

The deduction is equal to the sum of:

I. The lesser of:

I.1. The ‘combined qualified business income’ of the taxpayer, or

I.2. 20% of the excess of taxable income over the sum of any net capital gain

II. Plus the lesser of:

II.1. 20% of qualified cooperative dividends, or

II.2. Taxable income less net capital gain

The combined qualified business income is defined as:

I. The sum of:

a. The lesser of:

i. 20% of the taxpayer’s qualified business income, or

ii. The greater of:

1. 50% of the W-2 wages with respect to the business, or

2. 25% of the W-2 wages with respect to the business plus 2.5% of the unadjusted basis of all qualified property

II. Plus:

a. 20% of qualified REIT dividends, and

b. 20% of qualified publicly traded partnership (MLP) income

3. What is a qualified REIT dividend?

The term ‘qualified REIT dividend’ means any dividend from a real estate investment trust received during the taxable year which—

a) is not a capital gain dividend, and

b) is not qualified dividend income

4. What is qualified publicly traded partnership (MLP) income?

The term ‘qualified publicly traded partnership income’ means, with respect to any qualified trade or business of a taxpayer, the sum of—

a) the net amount of such taxpayer’s allocable share of each qualified item of income, gain, deduction, and loss from a publicly traded partnership which is not treated as a corporation under section 7704(c), plus

b) any gain recognized by such taxpayer upon disposition of its interest in such partnership to the extent such gain is treated as an amount realized from the sale or exchange of property other than a capital asset under section 751(a).

5. What is a qualified cooperative dividend?

The term ‘qualified cooperative dividend’ means any patronage dividend, any per-unit retain allocation, and any qualified written notice of allocation, or any similar amount received from an organization described in subparagraph (B)(ii), which—

a) is includible in gross income, and

b) is received from—

i. an organization or corporation described in section 501(c)(12) or 1381(a), or

ii. an organization which is governed under this title by the rules applicable to cooperatives under this title before the enactment of subchapter T.

6. What is Qualified Business Income (QBI)?

Qualified business income means the net amount of qualified items of income, gain, deduction, and loss with respect to the qualified trade or business of the taxpayer only to the extent they are effectively connected with the conduct of a trade or business within the United States (includes Puerto Rico). It does not include:

· Investment income (capital gains, dividends and/or interest)

· Reasonable compensation (W-2 wages) paid to an S-Corp owner

· Guaranteed payments to a partner for services rendered with respect to the trade of business

· Any amount paid or incurred by a partnership to a partner who is acting other than in his or her capacity as a partner for services

7. What is a qualified trade or business?

A qualified trade or business means any trade or business other than a specified service trade or business and other than the trade or business of being an employee. It includes any activity carried on for the production of income from selling goods or performing services.

8. What is a specified service trade or business?

A specified service trade or business means any trade or business involving the performance of services in the fields of health, law, accounting, actuarial science, performing arts, consulting, athletics, financial services, brokerage services, including investing and investment management, trading, or dealing in securities, partnership interests, or commodities, and any trade or business where the principal asset of such trade or business is the reputation or skill of one or more of its employees. The definition has been amended to remove the fields of engineering and architecture.

1. How does the W-2 limitation apply when taxable income is in excess of the threshold?

Congress has enacted W-2 and capital limitations to prevent individuals who are paid for regular services (w-2) to setup a pass-thru entity for the same service (1099) and get a 20% QBI deduction.

Example 1: Apple’s CEO Tim Cook is excited about the new 20% QBI deduction and decides to resign as an employee and provide consultancy services to the company using a single-member LLC under California law with no employees or qualified assets. He would like his $10 million annual salary to be taxed at an effective rate of 29.6% after the deduction instead of 37% that he currently pays without it.

During tax season, Tim realizes that his deduction is a BIG ZERO – here’s why:

QBI is the lesser of:

20% of Tim’s qualified business income = $2 million, or

The greater of:

50% of the W-2 wages with respect to the business = 0, or

25% of the W-2 wages with respect to the business plus 2.5% of the unadjusted basis of all qualified property = 0

The QBI deduction is designed to provide a break to businesses with payroll and/or qualified assets.

Example 2: John Smith’s allocable share of partnership/S-Corp earnings and expenses are as follows:

Net income $10 million

Unadjusted basis of depreciable property $10 million

W-2 wages $80 million

John’s QBI deduction is $2 million which will be calculated as follows:

The lesser of:

20% of John’s qualified business income = $2 million, or

The greater of:

50% of the W-2 wages allocable to John = $40 million, or

25% of the W-2 wages allocable to John (20 million) plus 2.5% of the unadjusted basis of all qualified property ($250k) = $20.25 million

2. Who determines the allocable share of W-2?

W-2 wages are wages paid to an employee (including owners) and would include any Section 401(k) elective deferrals or other deferred compensation. It does not include payments made to independent contractors.

Sole-proprietors: There is no allocation if you are the sole owner of a business and in such cases the number used for the calculation would be any wages paid with respect to the trade or business.

S-Corps: For a shareholder in an S corporation, Section 1366 and Section 1377 require that all items of an S corporation be allocated pro-rata, on a per-share/per-day basis.

Partnerships: Under Section 704(b), a partnership is allowed to ‘specially allocate’ different items of gain, loss and deductions amongst its partners at different percentages. However, under The TCJA, the partner’s allocable share of W-2 wages is required to be determined in the same manner as the partner’s share of wage expenses. For example, if a partner is allocated a deductible amount of 10 percent of wages paid by the partnership to employees for the taxable year, the partner is required to be allocated 10 percent of the W-2 wages of the partnership for purposes of calculating the wage limit under this deduction.

3. What is qualified property? Does it help individuals that own rental properties?

Qualified property means tangible property of a character subject to depreciation that is held by, and available for use in, the qualified trade or business at the close of the taxable year, and which is used in the production of qualified business income, and for which the depreciable period has not ended before the close of the taxable year. The depreciable period with respect to qualified property of a taxpayer means the period beginning on the date the property is first placed in service by the taxpayer and ending on the later of:

(a) The date 10 years after that date, or

(b) The last day of the last full year in the applicable recovery period that would apply to the property under section 168 (without regard to section 168(g)).

For the purposes of Section 199A, the unadjusted (non-depreciated) value of property will be used in computing the capital limitation if taxable income is above the threshold.

Example: Rick is a sole-proprietor and owns a residential rental property that he purchased 10 years ago for $275,000. Based on the Modified Accelerated Cost Recovery System (MACRS), his adjusted basis for tax purposes today is $175,000 ($275,000/27.5 years = $10k/year X 10 years = $100,000 total depreciation). However, in computing his capital limitation, he would use his unadjusted basis of 275k resulting in a potential QBI deduction of $6,875 ($275k X 2.5%).

Challenge question: What would Rick’s QBI deduction be if he earned $100,000 from his rental activity this year?

4. What is the ‘Phase-in’ range and how much can you deduct if you’re in it?

Qualified Business or Trade: you are in the phase-in range if your taxable income is between the $315,000 to $415,000 (MFJ) threshold amounts. Your deduction is ‘phased-in’ depending on how far in the range you are on a percentage basis. You’ll also have to take into account W-2 and capital limits, but not fully.

Example: Steve is married and earned $300,000 from his S-Corp this year. His allocable share of W-2 wages were $40,000 and ended up with taxable income of $375,000.

Deduction if under the threshold: $60,000 (20% of $300,000)

Deduction if above the threshold: $20,000 (greater of 50% of $40,000 or 25% of $40,000 plus 2.5%)

So if the W-2 limitations had applied, Steve would have been entitled to a deduction of only $20,000. This means that if taxable income had been $315,000 or less, the new law would have given Steve a break in the form of $40,000 of additional deduction ($60,000 - $20,000). This is known as the "excess amount" in Section 199A.

Deduction if within the phase-in range: the $40,000 excess amount will be reduced by the percentage by which Steve is in the phase-in range. Since Steve’s taxable income is $375,000, he is $60,000 into the $100,000 range which means he will lose 60% of the excess amount and thus will only be entitled to a $36,000 final deduction, calculated as follows:

20% QBI 60,000

Excess amount of $40,000 reduced by 60% (24,000)

Final deduction: 36,000

Specified service trade or business: same facts as the example above but now let’s assume that Steve is a lawyer and so falls under the definition of a specified service trade or business. Unlike above, there is no excess amount since Steve would not have been able to claim a deduction if his taxable income was above the threshold. He is 60% into the phase-out range and this means that his applicable percentage is 40%. Hence, he is only entitled to take into account 40% of his allocable share of QBI, W-2 wages and basis of assets in computing the deduction.

Apply the formula:

The lesser of:

i. 20% of QBI = $24,000 (120K X 20%)

ii. The greater of:

1. 50% of W-2 wages = $8,000 (16K X 50%), or

2. 25% of W-2 wages plus 2.5% basis = $4,000 (16K X 25% + $0)

The excess amount in this case is $16,000 (24k – 8k) and as such Steve should lose 60% of the excess amount calculated as follows:

20% QBI based on allocable percentage 24,000

Excess amount of $16,000 reduced by 60% (9,600)

Final deduction: 14,400